Finance Cost Meaning In Accounting - Chapter 9 Marginal And Absorption Costing - Finance costs are also known as financing costs and borrowing costs.. Essentially, the cost benefit principle is a common sense rule. Companies finance their operations either through equity financing or through borrowings and loans. Home » accounting dictionary » what is a cost? It is concerned with actual costs incurred and the estimation of future costs. Ias 23 was reissued in march 2007 and applies to annual periods beginning.

Cost accounting is an indirect part of financial accounting and a direct part of management accounting. One is called direct costs and the other is called indirect costs. Cost includes all costs necessary to get an asset in place and ready for use. A notable exception to this rule is the recording of marketable securities, which are recorded according to their market value.the historical cost usually bears little or no relationship. Direct costs are those expenses or costs that can be directly associated or contributed with a product, service, department, or cost object.

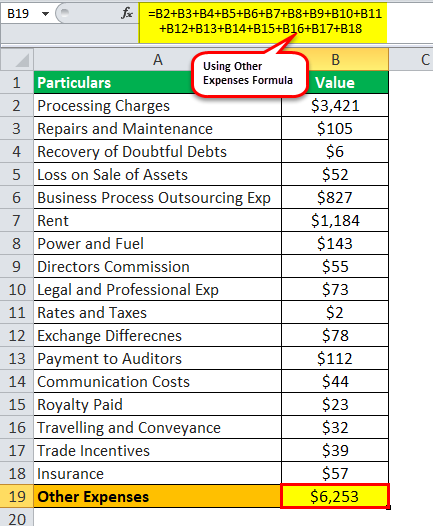

Other Expenses Definition List Of Other Expenses With Examples from cdn.wallstreetmojo.com Internal managers, rather than auditors, use cost accounting most of the time to identify aspects of their company where costs can be cut. For example, if a business has revenues of $1,000 and direct costs of $800, then it has a residual amount of $200 that can be contributed to the payment of fixed costs. Accounting cost, like accounting profit, follows the basic principles of accounting 101. Direct costs are any costs that vary directly with revenues, such as the cost of materials and commissions. Financial costing and management accounting are each prepared by different sets of rules and used by different parties. This can range from the cost it takes to finance a mortgage on a house, to finance a car loan through a bank, or to finance a student loan. Cost accounting primarily deals with collection, analysis of relevant cost data for interpretation and presentation for various problems of management. Cost accounting accounts for the costs of a product, a service or an operation.

Finance costs are also known as financing costs and borrowing costs.

Cost includes all costs necessary to get an asset in place and ready for use. Controlling the money being spent is the main aim of cost accounting while the primary purpose of financial accounting is to record all the transactions taking place in the company so that statements can be made. In other words, financial information is not free. A cost is an expenditure required to produce or sell a product or get an asset ready for normal use. An accounting cost is recorded in the ledgers of a business, so the cost appears in an entity's financial statements. Cost definition in accounting, cost is defined as the cash amount (or the cash equivalent) given up for an asset. Other borrowing costs are recognised as an expense. Ias 23 was reissued in march 2007 and applies to annual periods beginning. Financing cost (fc), also known as the cost of finances (cof), is the cost, interest, and other charges involved in the borrowing of money to build or purchase assets. Cost accounting a branch of accounting that observes and calculates the actual costs of a company's operations. It's exactly what it sounds like—the actual cost. Both cost accounting vs financial accounting can be used together to reduce costs and increase the profitability of a firm. Financial accounting is an accounting system that captures the records of financial information about the business to show the correct financial.

Cost accounting is the process of accounting from the point at which expenditure is incurred or committed to the establishment of its ultimate relationship with cost centers and cost units. In other words, financial information is not free. With the new costing techniques introduced by cost accounting, now total product costs are divided into two different categories or types. An accounting cost is recorded in the ledgers of a business, so the cost appears in an entity's financial statements. Cost definition in accounting, cost is defined as the cash amount (or the cash equivalent) given up for an asset.

Cost Accounting Wikipedia from upload.wikimedia.org A cost is an expenditure required to produce or sell a product or get an asset ready for normal use. Financing cost (fc), also known as the cost of finances (cof), is the cost, interest, and other charges involved in the borrowing of money to build or purchase assets. In the generally accepted accounting principles, the original cost of an asset on a balance sheet.many assets, particularly illiquid assets, are recorded on a balance sheet according to their historical cost. In other words, financial information is not free. According to definition given by cima, london cost accounting is the process of accounting for cost from the point at which expenditure is incurred to the establishment of its ultimate relationship with cost centres and cost units. Cost accounting methods follow gaap standards while managerial accounting data and reports can be in whatever form the managers need to analyze operations and make decisions. This can range from the cost it takes to finance a mortgage on a house, to finance a car loan through a bank, or to finance a student loan. They are also known as finance costs or borrowing costs. a company funds its operations using two different sources:

They are also known as finance costs or borrowing costs. a company funds its operations using two different sources:

Financial costing and management accounting are each prepared by different sets of rules and used by different parties. Financing costs are defined as the interest and other costs incurred by the company while borrowing funds. Accounting cost, like accounting profit, follows the basic principles of accounting 101. If an accounting cost has not yet been consumed and is equal to or greater than the capitalization limit of a business, the cost is recorded in the balance sheet. Ias 23 requires that borrowing costs directly attributable to the acquisition, construction or production of a 'qualifying asset' (one that necessarily takes a substantial period of time to get ready for its intended use or sale) are included in the cost of the asset. Cost accounting is a form of managerial accounting that aims to capture a company's total cost of production by assessing the variable costs of each step of production as well as fixed costs, such. Cost accounting ensures that the costs involved in business operations are reduced and it even reflects the actual picture of a company's business operations and it is calculated at the discretion of the management whereas financial accounting is done with the purpose of disclosing the right information and that too in a reliable and an accurate manner. It is concerned with actual costs incurred and the estimation of future costs. For example, if a business has revenues of $1,000 and direct costs of $800, then it has a residual amount of $200 that can be contributed to the payment of fixed costs. The cost benefit principle or cost benefit relationship states that the cost of providing financial information in the financial statements must not outweigh the benefit of that information to the users. A notable exception to this rule is the recording of marketable securities, which are recorded according to their market value.the historical cost usually bears little or no relationship. With the new costing techniques introduced by cost accounting, now total product costs are divided into two different categories or types. Cost accounting is the process of accounting from the point at which expenditure is incurred or committed to the establishment of its ultimate relationship with cost centers and cost units.

Direct costs are any costs that vary directly with revenues, such as the cost of materials and commissions. In simpler terms, accounting cost is the overall cost of anything your business has paid for. In the generally accepted accounting principles, the original cost of an asset on a balance sheet.many assets, particularly illiquid assets, are recorded on a balance sheet according to their historical cost. Cost accounting cannot lead to financial accounting, but financial accounting is the basis of cost accounting. This can range from the cost it takes to finance a mortgage on a house, to finance a car loan through a bank, or to finance a student loan.

How Operating Expenses And Cost Of Goods Sold Differ from www.investopedia.com Economic costs include both the explicit and implicit costs of an action. For example, if a business has revenues of $1,000 and direct costs of $800, then it has a residual amount of $200 that can be contributed to the payment of fixed costs. Financing cost (fc), also known as the cost of finances (cof), is the cost, interest, and other charges involved in the borrowing of money to build or purchase assets. Cost accounting is a form of managerial accounting that aims to capture a company's total cost of production by assessing the variable costs of each step of production as well as fixed costs, such. It is concerned with actual costs incurred and the estimation of future costs. According to definition given by cima, london cost accounting is the process of accounting for cost from the point at which expenditure is incurred to the establishment of its ultimate relationship with cost centres and cost units. With the new costing techniques introduced by cost accounting, now total product costs are divided into two different categories or types. Ias 23 was reissued in march 2007 and applies to annual periods beginning.

Ias 23 was reissued in march 2007 and applies to annual periods beginning.

Financial accounting is an accounting system that captures the records of financial information about the business to show the correct financial. Cost includes all costs necessary to get an asset in place and ready for use. With the new costing techniques introduced by cost accounting, now total product costs are divided into two different categories or types. Economic costs include both the explicit and implicit costs of an action. The cost benefit principle or cost benefit relationship states that the cost of providing financial information in the financial statements must not outweigh the benefit of that information to the users. Internal managers, rather than auditors, use cost accounting most of the time to identify aspects of their company where costs can be cut. Accounting cost, like accounting profit, follows the basic principles of accounting 101. It is concerned with actual costs incurred and the estimation of future costs. They are also known as finance costs or borrowing costs. a company funds its operations using two different sources: Financial accounting is a branch of accounting that. Cost accounting is an accounting process that measures all of the costs associated with production, including both fixed and variable costs. Cost accounting is an accounting system, through which an organization keeps the track of various costs incurred in the business in production activities. Actual cost is an accounting term that means the amount of money that was paid to acquire a product or asset.

:max_bytes(150000):strip_icc()/dotdash_Final_How_operating_expenses_and_cost_of_goods_sold_differ_Sep_2020-01-558a19250f604ecabba2901d5f312b31.jpg)